Availability of capital is a necessary and sufficient condition for the creation and further functioning of the enterprise. Proper management of an authorized capital of JSC provides a high level of profitability and development. Reduction of the authorized capital of the company - one of the financial management of the company leverage.

Rights and obligations of society

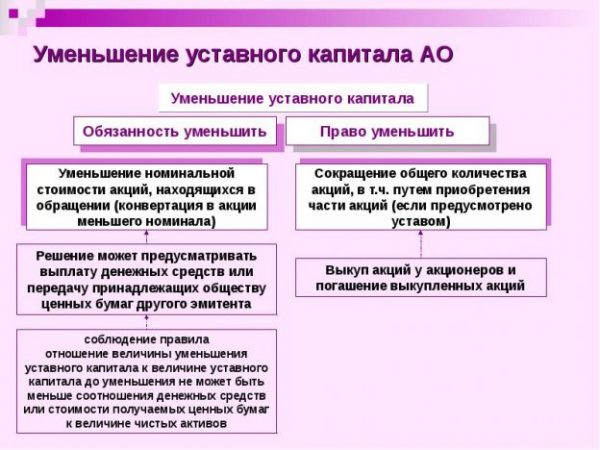

To achieve the company and ensure the rights of holders of shares of the law allows them to make a decision on reduction of the share capital, at its discretion. Typically used two versions:

To achieve the company and ensure the rights of holders of shares of the law allows them to make a decision on reduction of the share capital, at its discretion. Typically used two versions:

- purchase of shares of the company with further repayment (It is regulated by the articles of association);

- revaluation of securities by reducing their nominal value.

Bring the issue to the consideration of the meeting may be the board of directors. Assembly adopted a resolution by a majority vote of those present (75% «For»). The state registration - a mandatory procedure for the processing solutions.

The legislator has limited the scope of the Criminal Code of reducing the size of the company's assets, and established a ban on the procedure in the following cases:

- in the presence of outstanding shares as a result of the placement;

- passing by the bankruptcy proceedings;

- the requirement of owners for the purchase of their shares is not fulfilled (Article 75 of the JSC Law);

- the payment of dividends to the owners is not completed;

- the size of the company's assets does not meet the legal requirements for the reduction of the Criminal Code.

Reduction of the share capital is necessarily spent in the following cases:

- Company not promptly repaid the shares purchased from the owners;

- not all of the placed securities paid at the time of the Criminal reduction procedures;

- the ratio of capital assets does not meet the requirements of the law.

If the SA does not resolve the non-compliance and will not reduce the amount of the authorized fund, its activities may be terminated in court.

The goal of reducing the authorized capital

the owners interest in reducing the size of the Criminal Code is to obtain profits. source of income is the purchase and subsequent cancellation by redemption of shares of the company. The Supervisory Board sets the amount of compensation for each security.

In practice, the owners prefer to spend the capital reduction by revaluation of shares with a decrease of their cost. The payment is made within the total amount of funds, intended to compensate.

In practice, the owners prefer to spend the capital reduction by revaluation of shares with a decrease of their cost. The payment is made within the total amount of funds, intended to compensate.

the Company capital reduction used by large shareholders to buy up additional securities package. This possibility appears at the output of the minority shareholders of the company due to the sale of all shares.

The company's interest in reducing the volume defined by the Criminal Code of the current financial situation and the ability to prevent undesirable consequences. possible targets:

- prevent the fall in the value of the enterprise's assets in relation to the statutory fund;

- to compensate for losses by creating an imaginary income (Improved sanitation profit);

- Purchase of treasury securities in order to maintain their market price;

- method of reducing the mandatory minimum net assets in the conditions of market stagnation.

Grounds for reducing the Criminal Code

Security holders may request redemption of their shares in the following cases:

- they voted against the reorganization of the company;

- owners were against holding a particularly large commercial transactions;

- they did not support charter change, limiting their rights.

This right is guaranteed by Article 75 of them by the JSC Law. Ransom is the reason for the start of the Criminal Code of volume reduction procedure. The order provides for reorganization of the company redeemed all shares, which have been acquired at the request of their respective owners, at the time of redemption. If the securities are redeemed by the company for other reasons, she is entitled to during the year to dispose of them. A year later, a meeting of shareholders shall decide on the reduction and elimination of the Criminal Code of the shares.

The sequence of reduction of the authorized capital

Step by step instructions reduce the share capital:

- Determination of the current value of the shares. Conducted by an independent appraiser.

- The issue of reducing the Criminal Code tabled by the Board of Directors.

- For decision-making meeting held owners. The resolution approved by a majority of votes (75%).

- Sending R14002 form for registration (given three days).

- Publication in the press of the two posts on the reduction of the Criminal Code - one month.

- Assembly resolution approved by the board of directors.

- conducted emission, sale and registration of the issue.

- Registered new charter.

To reduce the Criminal Code through the purchase of shares and their subsequent redemption must perform these steps:

- The majority of votes at the meeting to approve the buying of shares.

- Officially notify the Federal Tax Service and creditors.

- To distribute to shareholders an offer.

- On the basis of the final report on the distribution of shares and the resolution of owners meeting to make changes to the statutory documents.

Registration of changes

after 90 days after the adoption of the resolution on decreasing the authorized capital amount necessary to amend the articles of association, contact the registrar. When a need to have:

after 90 days after the adoption of the resolution on decreasing the authorized capital amount necessary to amend the articles of association, contact the registrar. When a need to have:

- An application for amendment (filling the sample in 2017 year can be found on specialized sites);

- Protocol owners Assembly resolution on reducing the volume of the Criminal Code;

- charter capital amount with change (2 эkz.);

- proof of payment of the fee.

Accounting and taxes while reducing the Criminal Code

Accounting while reducing the authorized fund should reflect all transactions, held securities. Appropriate wiring determined by the selected method of reducing.

If as a result of reductions in statutory fund assets exceeded the size of the Criminal Code, then with the excess amount must be paid by a tax (A letter from the Federal Tax Service 06.09.2012 № AS-4-3 / 14878).

However, in the case of involuntary downgrade, this difference is not included in non-operating income and the tax is not charged.